The hardware and bandwidth for this mirror is donated by METANET, the Webhosting and Full Service-Cloud Provider.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]metanet.ch.

dfms provides a user friendly and computationally efficient approach to estimate linear Gaussian Dynamic Factor Models in R. The package is not geared at any specific application, and can be used for dimensionality reduction, forecasting and nowcasting systems of time series. The use of the package is facilitated by a comprehensive set of methods to explore/plot models and extract results.

This vignette walks through the main features of the package. The data provided in the package in xts format is taken from Banbura and Modugno (2014)1, henceforth BM14, and covers the Euro Area from January 1980 through September 2009.

# Using the monthly series from BM14

dim(BM14_M)

#> [1] 357 92

range(index(BM14_M))

#> [1] "1980-01-31" "2009-09-30"

head(colnames(BM14_M))

#> [1] "ip_total" "ip_tot_cstr" "ip_tot_cstr_en" "ip_constr" "ip_im_goods"

#> [6] "ip_capital"

plot(scale(BM14_M), lwd = 1)

The data frame BM14_Models provides information about

the series2, and the various models estimated by

BM14.

head(BM14_Models, 3)

#> series

#> 1 ip_total

#> 2 ip_tot_cstr

#> 3 ip_tot_cstr_en

#> label

#> 1 IP-Total Industry - Working Day and Seasonally Adjusted

#> 2 IP-Total Industry (Excluding Construction) - Working Day and Seasonally Adjusted

#> 3 IP-Total Industry Excluding Construction and MIG Energy - Working Day and Seasonally Adjusted

#> code freq log_trans small medium large

#> 1 sts.m.i5.Y.PROD.NS0010.4.000 M TRUE FALSE FALSE TRUE

#> 2 sts.m.i5.Y.PROD.NS0020.4.000 M TRUE TRUE TRUE TRUE

#> 3 sts.m.i5.Y.PROD.NS0021.4.000 M TRUE FALSE FALSE TRUE

# Using only monthly data

BM14_Models_M <- subset(BM14_Models, freq == "M")Prior to estimation, all data is differenced by BM14, and some series

are log-differenced, as indicated by the log_trans column

in BM14_Models. In general, dfms uses a stationary

Kalman Filter with time-invariant system matrices, and therefore expects

data to be stationary. Data is also scaled and centered3 in the main

DFM() function, thus this does not need to be done by the

user.

library(magrittr)

# log-transforming and first-differencing the data

BM14_M[, BM14_Models_M$log_trans] %<>% log()

BM14_M_diff <- diff(BM14_M)

plot(scale(BM14_M_diff), lwd = 1)

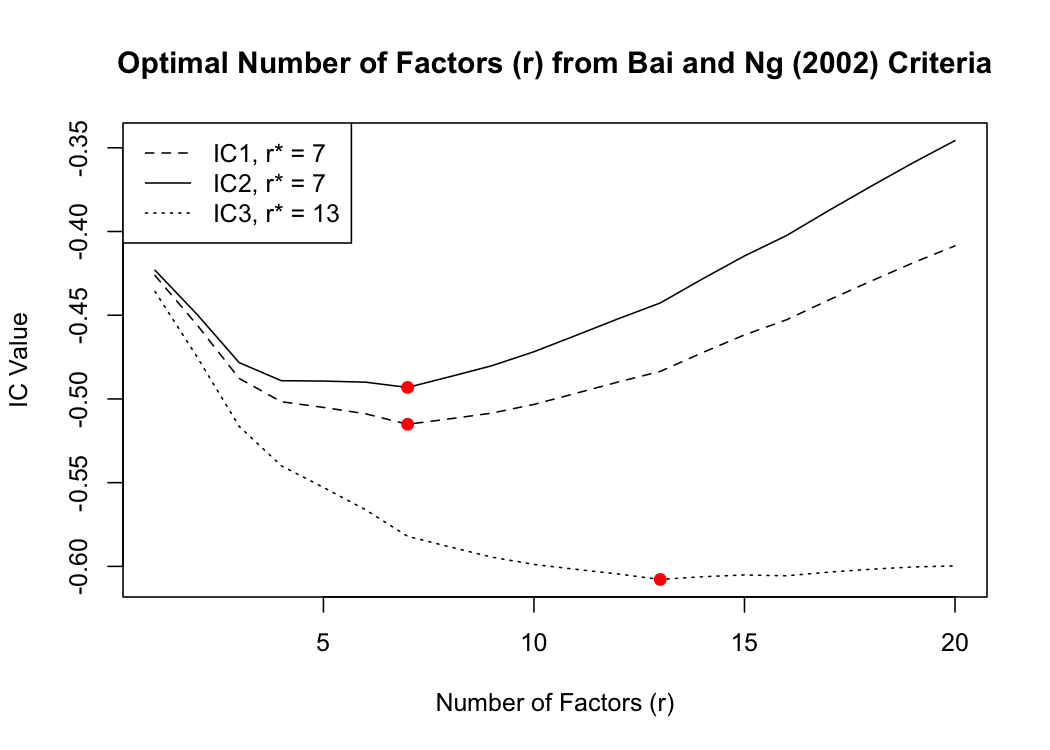

Before estimating a model, the ICr() function can be

applied to determine the number of factors. It computes 3 information

criteria proposed in Bai and NG (2002)4, whereby the second

criteria generally suggests the most parsimonious model.

ic <- ICr(BM14_M_diff)

#> Missing values detected: imputing data with tsnarmimp() with default settings

print(ic)

#> Optimal Number of Factors (r) from Bai and Ng (2002) Criteria

#>

#> IC1 IC2 IC3

#> 7 7 13

plot(ic)

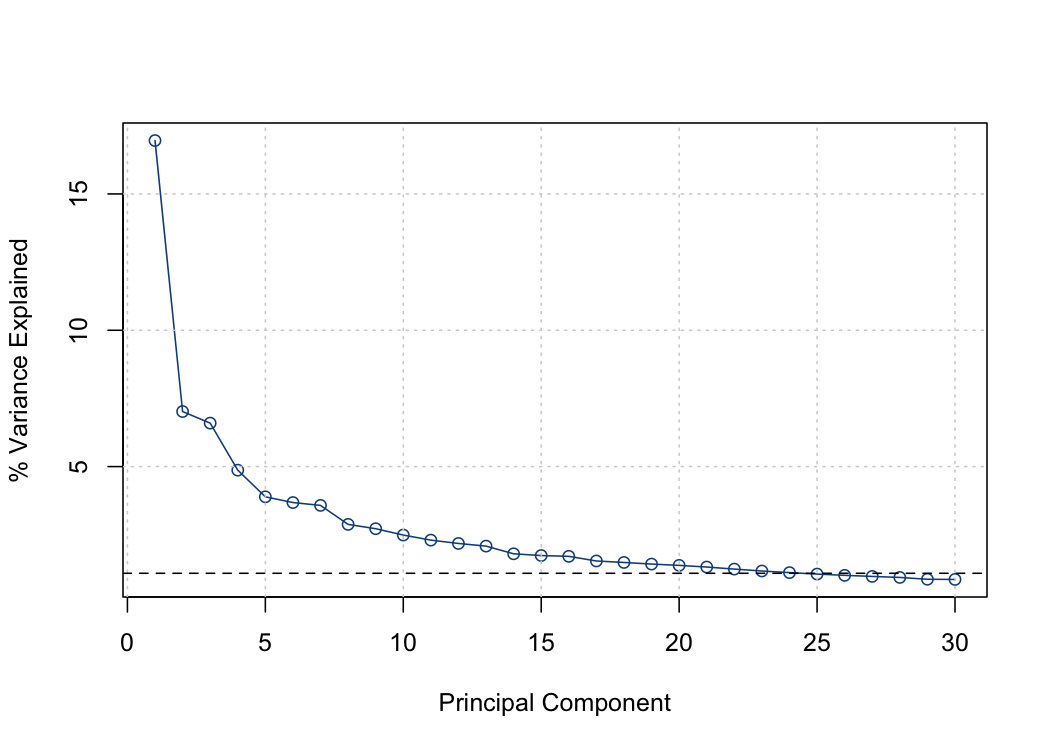

Another option is to use a Screeplot to gauge the number of factors

by looking for a kink in the plot. A mathematical procedure for finding

the kink was suggested by Onatski (2010)5, but this is currently

not implemented in ICr().

Based on both the information criteria and the Screeplot, I gauge

that a model with 4 factors should be estimated, as factors, 5, 6 and 7

do not add much to the explanatory power of the model. Next to the

number of factors, the lag order of the factor-VAR of the transition

equation should be estimated (the default is 1 lag). This can be done

using the VARselect() function from the vars

package, with PCA factor estimates reported by ICr().

# Using vars::VARselect() with 4 principal components to estimate the VAR lag order

vars::VARselect(ic$F_pca[, 1:4])

#> $selection

#> AIC(n) HQ(n) SC(n) FPE(n)

#> 4 3 3 4

#>

#> $criteria

#> 1 2 3 4 5 6 7 8

#> AIC(n) 5.794184 5.585334 5.400083 5.370339 5.394026 5.379200 5.407519 5.403436

#> HQ(n) 5.882720 5.744698 5.630276 5.671360 5.765875 5.821878 5.921025 5.987770

#> SC(n) 6.016522 5.985541 5.978161 6.126287 6.327844 6.490887 6.697076 6.870863

#> FPE(n) 328.386797 266.501718 221.456225 215.003864 220.219244 217.067620 223.429380 222.685797

#> 9 10

#> AIC(n) 5.433963 5.476516

#> HQ(n) 6.089126 6.202507

#> SC(n) 7.079260 7.299683

#> FPE(n) 229.808426 240.084376The selection thus suggests we should estimate a factor model with \(r = 4\) factors and \(p = 3\) lags6. Before estimating the model I note that dfms does not deal with seasonality in series, thus it is recommended to also seasonally adjust data, e.g. using the seasonal package before estimation. BM14 only use seasonally adjusted series, thus this is not necessary with the example data provided.

Estimation can then simply be done using the DFM()

function with parameters \(r\) and

\(p\)7.

# Estimating the model with 4 factors and 3 lags using BM14's EM algorithm

model_m <- DFM(BM14_M_diff, r = 4, p = 3)

#> Converged after 26 iterations.

print(model_m)

#> Dynamic Factor Model: n = 92, T = 356, r = 4, p = 3, %NA = 25.8366

#>

#> Factor Transition Matrix [A]

#> L1.f1 L1.f2 L1.f3 L1.f4 L2.f1 L2.f2 L2.f3 L2.f4 L3.f1 L3.f2 L3.f3

#> f1 0.4139 -0.0122 0.7875 0.3325 -0.0914 -0.1474 0.1859 -0.3054 0.3228 -0.0710 0.0023

#> f2 -0.1358 0.2381 0.1742 0.2223 -0.0090 -0.1529 -0.0251 -0.0191 0.1530 0.1581 0.0549

#> f3 0.3392 0.2566 -0.0463 -0.4133 -0.1421 -0.0714 -0.2022 0.1173 -0.1204 0.0284 0.1685

#> f4 0.3268 0.1578 -0.1243 0.2149 0.0107 0.0064 -0.0746 -0.0236 -0.1655 -0.0427 -0.1069

#> L3.f4

#> f1 0.1806

#> f2 -0.0381

#> f3 0.1195

#> f4 0.0079

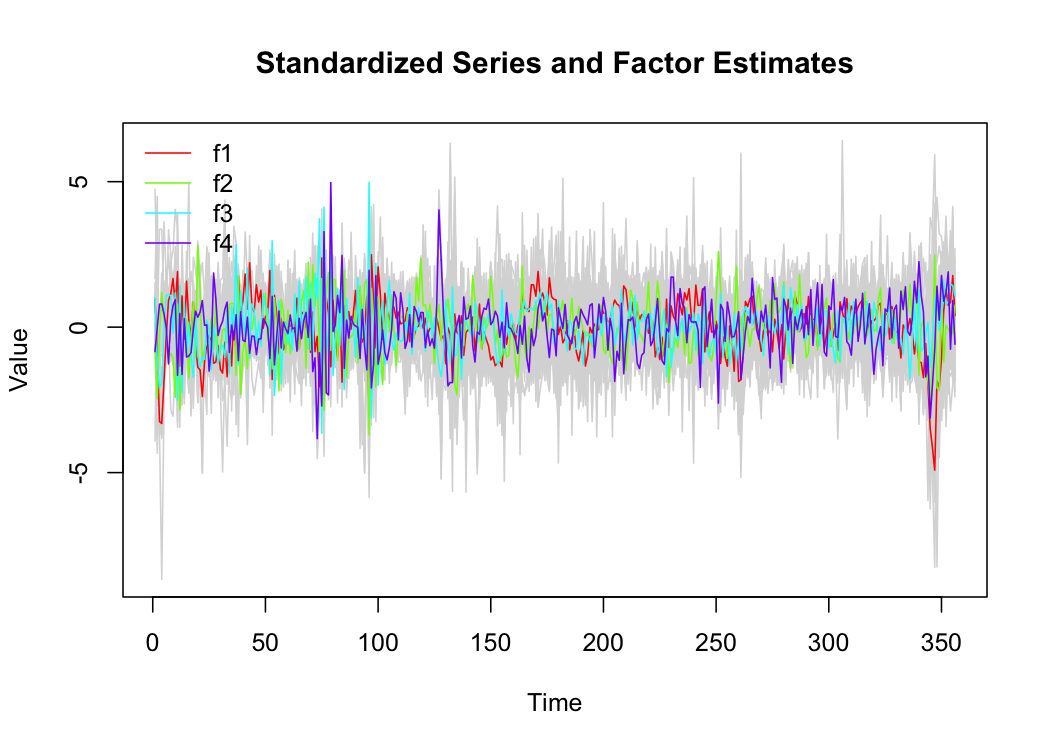

plot(model_m)

The model can be investigated using summary(), which

returns an object of class ‘dfm_summary’ containing the system matrices

and summary statistics of the factors and the residuals in the

measurement equation, as well as the R-Squared of the factor model for

individual series. The print method automatically adjusts the amount of

information printed to the data size. For large databases with more than

40 series, no series-level statistics are printed.

dfm_summary <- summary(model_m)

#> Warning in sqrt(1 - acm^2): NaNs produced

print(dfm_summary) # Large model with > 40 series: defaults to compact = 2

#> Dynamic Factor Model: n = 92, T = 356, r = 4, p = 3, %NA = 25.8366

#>

#> Call: DFM(X = BM14_M_diff, r = 4, p = 3)

#>

#> Summary Statistics of Factors [F]

#> N Mean Median SD Min Max

#> f1 356 -0.054 0.3333 4.6456 -20.9539 13.2308

#> f2 356 -0.031 -0.0728 2.6379 -9.317 6.9993

#> f3 356 -0.0504 0.0814 3.5123 -13.65 17.588

#> f4 356 -0.1345 -0.1719 2.4508 -9.8979 10.2893

#>

#> Factor Transition Matrix [A]

#> L1.f1 L1.f2 L1.f3 L1.f4 L2.f1 L2.f2 L2.f3 L2.f4 L3.f1 L3.f2

#> f1 0.4139 -0.01222 0.78747 0.3325 -0.091402 -0.147358 0.18593 -0.30539 0.3228 -0.07104

#> f2 -0.1358 0.23813 0.17418 0.2223 -0.009044 -0.152925 -0.02514 -0.01912 0.1530 0.15809

#> f3 0.3392 0.25655 -0.04625 -0.4133 -0.142128 -0.071381 -0.20221 0.11734 -0.1204 0.02844

#> f4 0.3268 0.15782 -0.12431 0.2149 0.010684 0.006446 -0.07456 -0.02356 -0.1655 -0.04269

#> L3.f3 L3.f4

#> f1 0.002269 0.180614

#> f2 0.054876 -0.038129

#> f3 0.168495 0.119479

#> f4 -0.106921 0.007872

#>

#> Factor Covariance Matrix [cov(F)]

#> f1 f2 f3 f4

#> f1 21.5818 1.9628* -4.9668* -1.5043*

#> f2 1.9628* 6.9585 -2.7590* -1.5049*

#> f3 -4.9668* -2.7590* 12.3359 2.9879*

#> f4 -1.5043* -1.5049* 2.9879* 6.0067

#>

#> Factor Transition Error Covariance Matrix [Q]

#> u1 u2 u3 u4

#> u1 9.3698 0.3902 -2.7169 -2.0670

#> u2 0.3902 5.3407 -1.0810 -0.7602

#> u3 -2.7169 -1.0810 7.2794 1.2365

#> u4 -2.0670 -0.7602 1.2365 4.1717

#>

#> Summary of Residual AR(1) Serial Correlations

#> N Mean Median SD Min Max

#> 92 -0.0314 -0.0657 0.3047 -0.5076 0.6918

#>

#> Summary of Individual R-Squared's

#> N Mean Median SD Min Max

#> 92 0.3783 0.3257 0.2866 0.0049 0.9976

# Can request more detailed printouts

# print(dfm_summary, compact = 1)

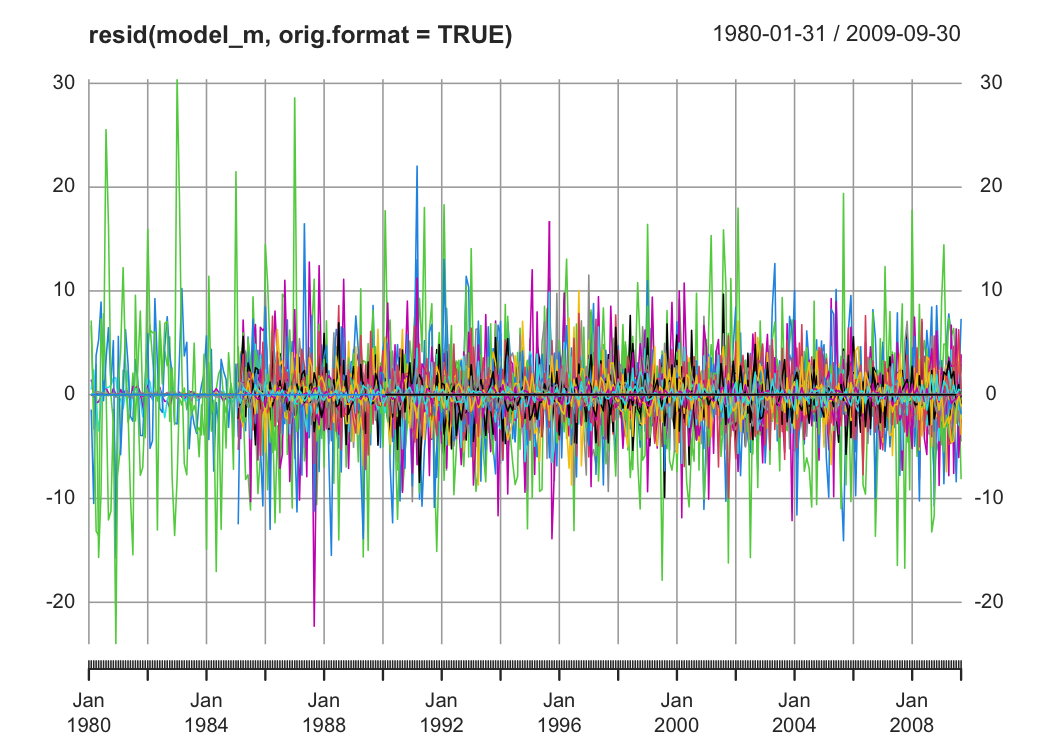

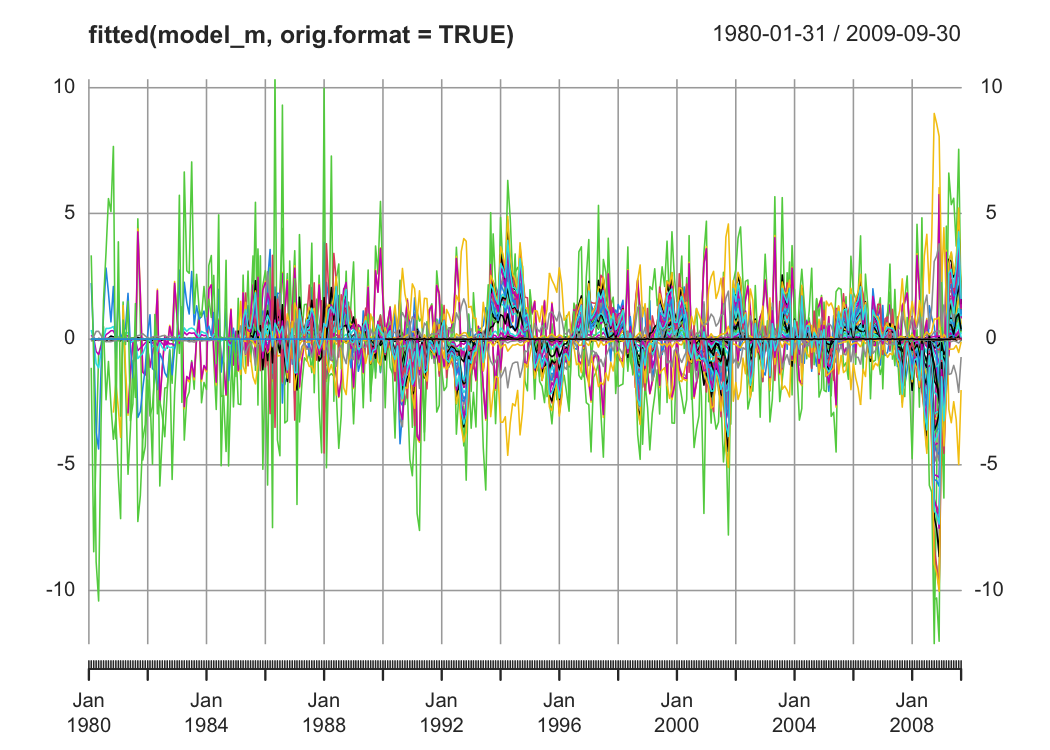

# print(dfm_summary, compact = 0)Apart from the model summary, the dfm methods

residuals() and fitted() return observation

residuals and fitted values from the model. The default format is a

plain matrix, but the functions also have an argument to return data in

the original (input) format.

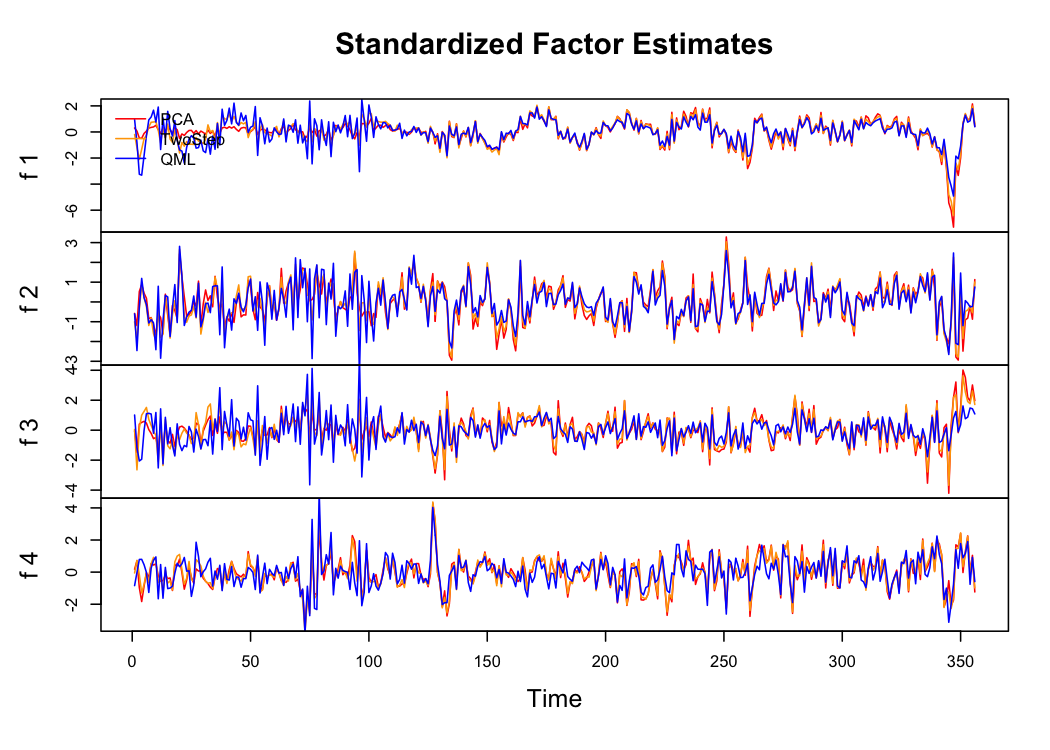

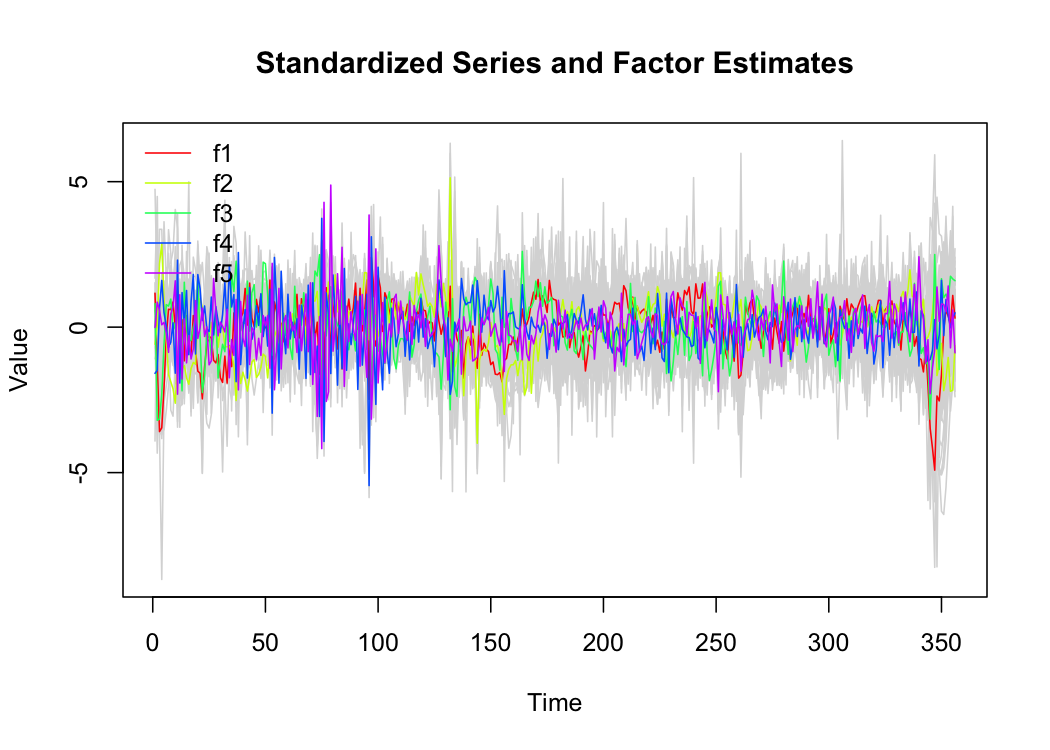

Another way to examine the factor model visually is to plot the

Quasi-Maximum-Likelihood (QML) factor estimates against PCA and Two-Step

estimates following Doz, Giannone and Reichlin (2011)8, where the Kalman

Filter and Smoother is run only once. Both estimates are also computed

by DFM() during EM estimation and can also be visualized

with plot.dfm.

The plot with the various estimates shows that the QML estimates are

more volatile in the initial periods where there are many missing

series, but less volatile in the latter periods. In general, QML

estimates may not always be superior across the entire data range to

Two-Step and PCA estimates. Often, Two-Step estimates also provide

similar forecasting performance, and are much faster to estimate using

DFM(BM14_M_diff, r = 4, p = 3, em.method = "none").

The factor estimates themselves can be extracted in a data frame

using as.data.frame(), which also provides various options

regarding the estimates retained and the format of the frame. It is also

possible to add a time variable from the original data (the default is a

sequence of integers).

# Default: all estimates in long format

head(as.data.frame(model_m, time = index(BM14_M_diff)))

#> Method Factor Time Value

#> 1 PCA f1 1980-02-29 1.2337752

#> 2 PCA f1 1980-03-31 0.3211015

#> 3 PCA f1 1980-04-30 -1.5238335

#> 4 PCA f1 1980-05-31 -1.5166031

#> 5 PCA f1 1980-06-30 -0.2327899

#> 6 PCA f1 1980-07-31 0.3928228DFM forecasts can be obtained with the predict() method,

which dynamically forecasts the factors using the transition equation

(default 10 periods), and then also predicts data forecasts using the

observation equation. Objects are of class ‘dfm_forecast’.

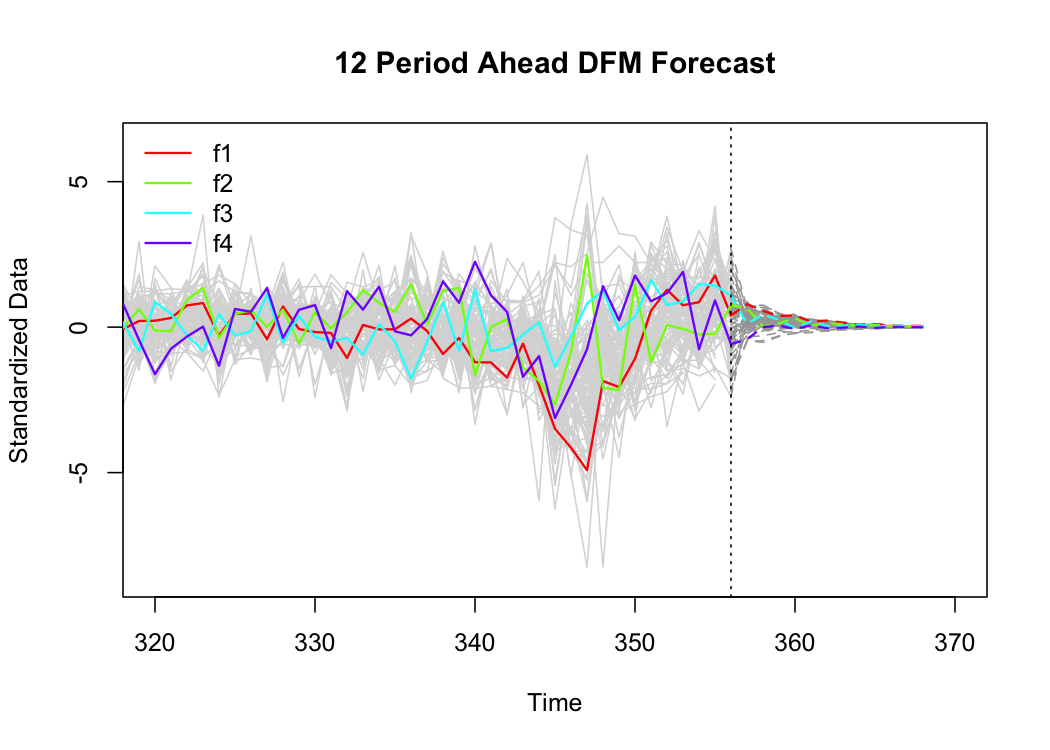

# 12-period ahead DFM forecast

fc <- predict(model_m, h = 12)

print(fc)

#> 12 Step Ahead Forecast from Dynamic Factor Model

#>

#> Factor Forecasts

#> f1 f2 f3 f4

#> 1 4.4600 0.7991 -0.0984 -0.2691

#> 2 4.1010 0.5169 0.8266 -0.3904

#> 3 2.3757 0.4360 0.9863 0.5066

#> 4 3.0793 0.7497 -0.7329 0.0622

#> 5 1.6748 0.2933 0.3500 0.3795

#> 6 1.3739 0.3297 0.0878 0.2092

#> 7 1.4066 0.4247 -0.2905 0.0570

#> 8 0.7346 0.1105 0.2751 0.2562

#> 9 0.8001 0.2191 -0.1221 0.0672

#> 10 0.5777 0.1661 -0.0318 0.0882

#> 11 0.3690 0.0714 0.0985 0.1017

#> 12 0.4077 0.1229 -0.0829 0.0208

#>

#> Series Forecasts

#> ip_total ip_tot_cstr ip_tot_cstr_en ip_constr ip_im_goods ip_capital ip_d_cstr ip_nd_cons

#> 1 0.9055 0.9232 0.9581 0.2297 0.9016 0.7424 0.6656 0.5287

#> ip_en ip_en_2 ip_manuf ip_metals ip_chemicals ip_electric ip_machinery ip_paper

#> 1 0.0300 0.0720 0.9686 0.6876 0.6051 0.7846 0.6228 0.5709

#> ip_plastic new_cars orders ret_turnover_defl ecs_ec_sent_ind ecs_ind_conf

#> 1 0.7460 0.1033 0.5756 0.0163 0.9179 0.9392

#> ecs_ind_order_book ecs_ind_stocks ecs_ind_prod_exp ecs_ind_prod_rec_m ecs_ind_x_orders

#> 1 0.8858 -0.6206 0.7372 0.6142 0.7822

#> ecs_ind_empl_exp ecs_cons_conf ecs_cons_sit_over_next_12 ecs_cons_exp_unempl

#> 1 0.6932 0.6451 0.5826 -0.5907

#> ecs_cons_gen_last_12m ecs_cstr_conf ecs_cstr_order_books ecs_cstr_empl_exp

#> 1 0.6125 0.3601 0.2798 0.2974

#> ecs_cstr_prod_recent ecs_ret_tr_conf ecs_ret_tr_bus_sit ecs_ret_tr_stocks

#> 1 0.2569 0.2343 0.1304 -0.0438

#> ecs_ret_tr_exp_bus ecs_ret_tr_empl ecs_serv_conf ecs_serv_empl_exp pms_comp_output

#> 1 0.2883 0.1717 0.5419 0.4216 0.5936

#> pms_comp_empl pms_pmi pms_manuf_empl pms_manuf_output pms_manuf_product pms_serv_out

#> 1 0.5765 0.6576 0.6838 0.5825 0.3972 0.4842

#> pms_serv_empl pms_serv_new_bus pms_serv_product urx empl_total empl_tot_xc empl_cstr

#> 1 0.3745 0.5237 0.3316 -0.4692 0.4548 0.2340 0.5819

#> empl_manuf extra_ea_trade_exp_val intra_ea_trade_exp_val extra_ea_trade_imp_val

#> 1 0.2549 0.3973 0.3731 0.2520

#> intra_ea_trade_imp_val us_ip us_urx us_empl us_retail_sales us_ip_manuf_exp us_cons_exp

#> 1 0.3477 0.4234 -0.3765 0.2862 0.2671 0.1714 0.1539

#> us_r3_m us_r10_year

#> 1 0.3824 0.3136

#> [ reached 'max' / getOption("max.print") -- omitted 11 rows and 22 columns ]These forecasts can also be visualized using a plot method. By default the entire series history is plotted along with the forecasts, thus it is often helpful to restrict the plot range. As with any stationary autoregressive model, the forecasts tend to zero quite quickly9.

By default, predict() uses the QML factor estimates (if

available). We can however also predict with PCA or TwoStep estimates

using, e.g., predict(model_m, h = 12, method = "2s").

The forecasts can be retrieved in data frame using

as.data.frame(). Again the method has various arguments to

control the output (factors, data, or both — default factors) and the

format of the frame.

# Factor forecasts in wide format

head(as.data.frame(fc, pivot = "wide"))

#> Time Forecast f1 f2 f3 f4

#> 1 1 FALSE 6.8690809 -1.34246514 3.441482 1.0535954

#> 2 2 FALSE -3.7001043 -8.58051260 -6.924850 6.8407922

#> 3 3 FALSE -17.3898728 -0.39832405 -5.701603 -4.0826421

#> 4 4 FALSE -17.7877846 3.48235068 -1.198272 -9.8978618

#> 5 5 FALSE -8.2124387 0.74239760 4.057838 -5.5472619

#> 6 6 FALSE -0.3234256 -0.09166592 5.033747 -0.9623612Since v0.3.0, dfms allows monthly and quarterly mixed

frequency estimation following Mariano & Murasawa (2003) and Banbura

& Modugno (2014). Quarterly variables should be to the right of the

monthly variables in the data matrix and need to be indicated using the

quarterly.vars argument. Quarterly observations should be

provided every 3rd period (months 3, 6, 9, and 12). Below, I estimate

the mixed frequency DFM, adding a factor to capture any idiosynchratic

dynamics in the quarterly series.

# Quarterly series from BM14

head(BM14_Q, 3)

#> gdp priv_cons invest export import empl prductivity capacity

#> 1980-03-31 2.632160 2.592850 2.516355 2.506821 2.505304 2.457959 NA NA

#> 1980-06-30 2.631821 2.592391 2.514986 2.503178 2.503075 2.458010 NA NA

#> 1980-09-30 2.631780 2.592931 2.514673 2.502228 2.503705 2.458013 NA NA

#> gdp_us

#> 1980-03-31 2.161499

#> 1980-06-30 2.159112

#> 1980-09-30 2.158896

# Pre-processing the data

BM14_Q[, BM14_Models$log_trans[BM14_Models$freq == "Q"]] %<>% log()

BM14_Q_diff <- diff(BM14_Q)

# Merging to monthly data

BM14_diff <- merge(BM14_M_diff, BM14_Q_diff)

# Estimating the model with 5 factors and 3 lags using BM14's EM algorithm

model_mq <- DFM(BM14_diff, r = 5, p = 3, quarterly.vars = colnames(BM14_Q))

#> Converged after 33 iterations.

print(model_mq)

#> Mixed Frequency Dynamic Factor Model

#> n = 101, nm = 92, nq = 9, T = 356, r = 5, p = 3

#> %NA = 29.7363, %NAm = 25.8366

#>

#> Factor Transition Matrix [A]

#> L1.f1 L1.f2 L1.f3 L1.f4 L1.f5 L2.f1 L2.f2 L2.f3 L2.f4 L2.f5 L3.f1

#> f1 0.4038 -0.2905 0.5106 -0.3668 0.3582 -0.0201 0.1704 -0.1055 -0.3729 -0.2237 0.3403

#> f2 -0.1359 0.4813 -0.1610 -0.0835 0.0551 0.0894 -0.0312 0.0059 -0.0330 0.2461 0.1384

#> f3 0.1962 0.0884 0.3432 0.1038 -0.0821 -0.1337 -0.0121 -0.2337 0.0901 -0.1168 -0.0139

#> f4 -0.2052 -0.1555 0.1237 -0.0669 0.5170 0.0329 -0.0413 0.0692 -0.2223 -0.1077 0.0239

#> L3.f2 L3.f3 L3.f4 L3.f5

#> f1 -0.0910 0.0940 0.0106 0.1322

#> f2 0.2373 0.1304 -0.1657 0.0100

#> f3 -0.1081 0.1836 0.1080 -0.0727

#> f4 -0.1317 -0.0602 0.1138 -0.1394

#> [ reached 'max' / getOption("max.print") -- omitted 1 row ]

plot(model_mq)

By default, observation errors are assumed to be white noise.

However, in practice, idiosyncratic errors often exhibit serial

correlation. Setting idio.ar1 = TRUE models observation

errors as AR(1) processes: \(e_{it} = \rho_i

e_{i,t-1} + v_{it}\), where \(\rho_i\) is estimated for each series.

This option can be combined with mixed-frequency estimation. Since estimating AR(1) errors increases runtime, the examples below use the medium-sized dataset.

BM14_med_diff <- BM14_diff[, BM14_Models$medium]

Q_vars_med <- intersect(colnames(BM14_med_diff), colnames(BM14_Q))

# Mixed-frequency model with AR(1) idiosyncratic errors

model_mq_ar1 <- DFM(BM14_med_diff, r = 5, p = 3, idio.ar1 = TRUE,

quarterly.vars = Q_vars_med)

#> Converged after 26 iterations.

print(model_mq_ar1)

#> Mixed Frequency Dynamic Factor Model

#> n = 48, nm = 39, nq = 9, T = 356, r = 5, p = 3

#> %NA = 32.6135, %NAm = 24.0781

#> with AR(1) errors: mean(abs(rho)) = 0.262

#>

#> Factor Transition Matrix [A]

#> L1.f1 L1.f2 L1.f3 L1.f4 L1.f5 L2.f1 L2.f2 L2.f3 L2.f4 L2.f5 L3.f1

#> f1 1.3215 -0.5413 0.1691 -0.5893 0.1477 -0.5107 0.5863 0.1646 0.1568 -0.1492 0.0185

#> f2 -0.1156 0.4177 0.1762 -0.2619 0.0895 0.0889 -0.0066 0.0144 -0.0043 0.0285 -0.2113

#> f3 -0.2913 0.3117 0.3426 0.3239 -0.2416 1.1182 -1.0212 -0.1275 -0.4937 -0.1119 -0.9063

#> f4 0.1784 -0.0789 0.1831 0.0182 -0.2895 -0.3356 0.2854 -0.0259 -0.0285 -0.0916 0.1251

#> L3.f2 L3.f3 L3.f4 L3.f5

#> f1 -0.0343 -0.0809 -0.0262 -0.1292

#> f2 0.3440 -0.0407 0.1760 -0.1395

#> f3 0.6023 0.2533 0.0171 -0.1862

#> f4 -0.0359 -0.0976 0.1304 0.1229

#> [ reached 'max' / getOption("max.print") -- omitted 1 row ]The estimated AR(1) coefficients (\(\rho\)) for each series are stored in the

rho element of the model object. For most series, the AR(1)

coefficients are small, indicating little serial correlation in the

idiosyncratic errors after accounting for the common factors.

# AR(1) coefficients for the first 10 series

head(model_mq_ar1$rho, 10)

#> ip_tot_cstr ip_constr ip_im_goods ip_capital ip_d_cstr

#> -0.4930859 -0.3859705 -0.2902739 -0.3914880 -0.2668469

#> ip_nd_cons ip_en new_cars orders ret_turnover_defl

#> -0.3202793 -0.3268949 -0.4200600 -0.4316412 -0.4973194

# Summary of AR(1) coefficients

summary(model_mq_ar1$rho)

#> Min. 1st Qu. Median Mean 3rd Qu. Max.

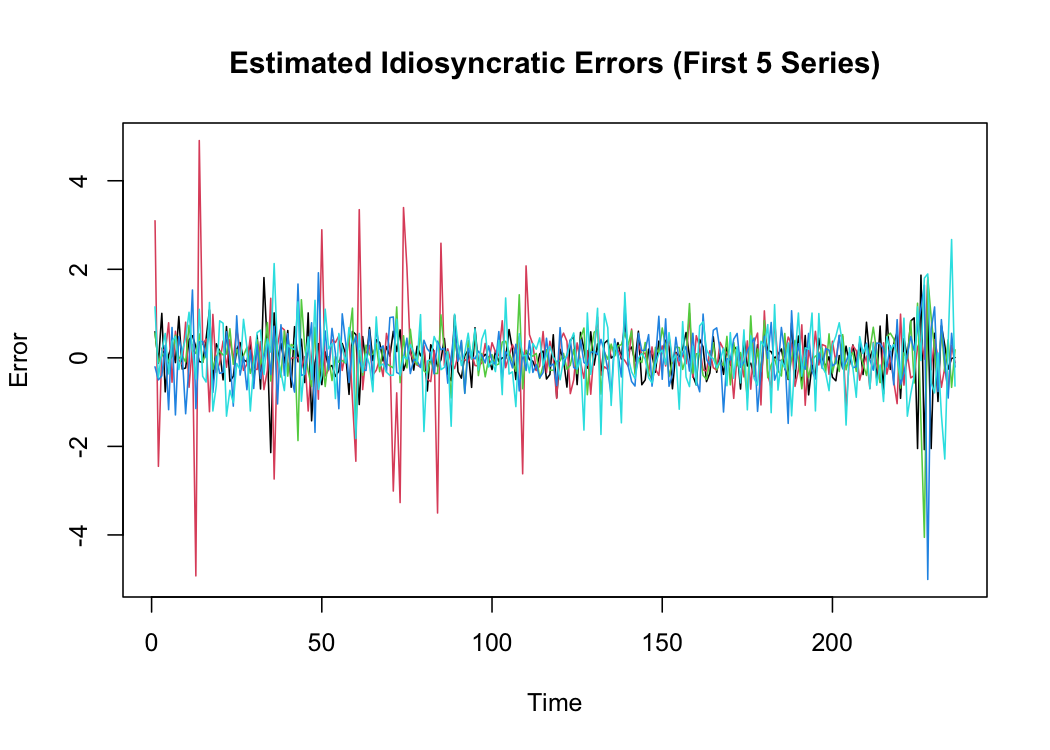

#> -0.60839 -0.28946 -0.13638 -0.08143 0.19829 0.67993The estimated observation errors are available in the e

element.

# Dimension of estimated errors

dim(model_mq_ar1$e)

#> [1] 356 48

# Plot estimated errors for first 5 monthly series

matplot(model_mq_ar1$e[-(1:120), 1:5], type = "l", lty = 1,

main = "Estimated Idiosyncratic Errors (First 5 Series)",

xlab = "Time", ylab = "Error")

In general, Doz et al. (2011, 2012) show that in the presence of serial correlation, the factors are still consistently estimated as \(n, T \to \infty\) using an exact DFM specification. Thus modeling serial correlation is particularly important in smaller samples. Banbura & Modugno (2014) also show that modeling the serial correlation improves forecast accuracy, but only at short horizons.

The news() function decomposes forecast revisions into

contributions from new data releases following Banbura and Modugno

(2014). The idea is to compare an old vintage (with ragged-edge missing

values) to a new vintage where some missing values are now observed. The

output reports the forecast revision for a target series (usually a

quarterly variable such as GDP not yet observed in the current period)

and decomposes the change in its DFM-based forecast into series

contributions.

Below, we use a medium-size mixed-frequency dataset, create a previous vintage, and compute news impacts for the quarterly targets.

# Create old vintage with ragged edge

model_mq_ar1$rm.rows # Previous model removed first row

#> [1] 1

X_old <- BM14_med_diff[-model_mq_ar1$rm.rows, ]

tail(X_old, 3) # See current ragged edge

#> ip_tot_cstr ip_constr ip_im_goods ip_capital ip_d_cstr ip_nd_cons

#> 2009-07-31 0.000285243 -0.002623227 0.0020305483 -0.002454670 0.0009548859 0.0004096236

#> ip_en new_cars orders ret_turnover_defl ecs_ec_sent_ind

#> 2009-07-31 0.0001183144 -0.0005719138 0.002943768 -0.0001764322 2.800003

#> ecs_ind_conf ecs_ind_prod_exp ecs_ind_x_orders ecs_ind_empl_exp ecs_cons_conf

#> 2009-07-31 2.100000 2.400001 1.100002 1.7999992 2.1

#> ecs_cstr_conf ecs_ret_tr_conf ecs_serv_conf ecs_serv_empl_exp pms_pmi pms_serv_out

#> 2009-07-31 0.2999992 3.6999998 2.299999 1.5 3.63 1.04

#> urx empl_total extra_ea_trade_exp_val extra_ea_trade_imp_val us_ip

#> 2009-07-31 0.1056456 NA 0.0007397515 -5.587142e-05 0.001372389

#> us_ip_manuf_exp us_cons_exp m3 loans ir_long ir_short

#> 2009-07-31 6 -6.0 3.041118e-04 -8.497176e-05 -0.20008969 -0.25295257

#> eer exr_usd euro325 dow_j raw_mat_en raw_mat_oil_fwd gdp

#> 2009-07-31 0.1361271 0.007124111 0.0006282595 0.000502753 -0.001999095 -0.01216823 NA

#> priv_cons invest export import empl prductivity capacity gdp_us

#> 2009-07-31 NA NA NA NA NA NA NA NA

#> [ reached 'max' / getOption("max.print") -- omitted 2 rows ]

(obscurr <- colnames(X_old)[is.finite(tail(X_old, 1))]) # Observe current

#> [1] "new_cars" "ecs_ec_sent_ind" "ecs_ind_conf" "ecs_ind_prod_exp"

#> [5] "ecs_ind_x_orders" "ecs_ind_empl_exp" "ecs_cons_conf" "ecs_cstr_conf"

#> [9] "ecs_ret_tr_conf" "ecs_serv_conf" "ecs_serv_empl_exp" "pms_pmi"

#> [13] "pms_serv_out" "us_ip_manuf_exp" "us_cons_exp" "ir_long"

#> [17] "ir_short" "eer" "exr_usd" "euro325"

#> [21] "dow_j" "raw_mat_en" "raw_mat_oil_fwd" "capacity"

# Set some observed values to NA

set.seed(1)

X_old[nrow(X_old), sample(obscurr, 10)] <- NA

# Also check series missing the previous observation and set some to NA

(obsprev <- colnames(X_old)[is.finite(tail(X_old, 2)[1, ])] |> setdiff(obscurr))

#> [1] "ip_tot_cstr" "ip_im_goods" "ip_capital" "ip_d_cstr"

#> [5] "ip_nd_cons" "ip_en" "ret_turnover_defl" "urx"

#> [9] "us_ip" "m3" "loans"

set.seed(1)

X_old[nrow(X_old), sample(obsprev, 4)] <- NA

# Estimating same DFM on old vintage

model_mq_ar1_old <- model_mq_ar1$call

model_mq_ar1_old$X <- quote(X_old)

model_mq_ar1_old$max.missing = 1 # No further row removals

print(model_mq_ar1_old)

#> DFM(X = X_old, r = 5, p = 3, idio.ar1 = TRUE, quarterly.vars = Q_vars_med,

#> max.missing = 1)

model_mq_ar1_old <- eval(model_mq_ar1_old)

#> Converged after 26 iterations.

# Compute news for "gdp" variable at the last period (t.fcst = nrow(X_old))

news_gdp <- news(model_mq_ar1_old, model_mq_ar1, target.vars = "gdp")

print(news_gdp)

#> DFM News

#> Target variable: gdp

#> Target time: 356

#> Old forecast: 1e-04

#> New forecast: 1e-04

#> Revision: 0

#> Standardized: FALSE

# Verifying the news decomposition

na.omit(news_gdp$news_df) |>

transform(test1 = news - (actual - forecast), test2 = impact - news * gain)

#> series actual forecast news gain gain_std

#> 8 new_cars -0.0002384109 -0.0002167886 -2.162227e-05 7.379485e-04 1.032980e-06

#> 11 ecs_ec_sent_ind 2.0000000000 1.9544155170 4.558448e-02 7.667486e-07 1.302062e-06

#> 13 ecs_ind_prod_exp 0.5000000000 2.6387291274 -2.138729e+00 -9.684502e-07 -2.125806e-06

#> 14 ecs_ind_x_orders 1.5000000000 0.9235600067 5.764400e-01 1.336228e-06 3.272888e-06

#> 16 ecs_cons_conf 3.0000000000 1.4263128445 1.573687e+00 6.372557e-07 9.474786e-07

#> 20 ecs_serv_empl_exp 1.3999996185 0.6240537062 7.759459e-01 3.695631e-07 9.496770e-07

#> 28 us_ip_manuf_exp -7.0000000000 6.2379822501 -1.323798e+01 -1.117836e-07 -9.664301e-07

#> impact test1 test2

#> 8 -1.595612e-08 0 0

#> 11 3.495184e-08 0 0

#> 13 2.071253e-06 0 0

#> 14 7.702555e-07 0 0

#> 16 1.002841e-06 0 0

#> 20 2.867610e-07 0 0

#> 28 1.479789e-06 0 0

#> [ reached 'max' / getOption("max.print") -- omitted 3 rows ]

# Now computing news for all quarterly variables

news_qvars <- news(model_mq_ar1_old, model_mq_ar1, target.vars = Q_vars_med)

print(news_qvars)

#> DFM News (Multiple Targets)

#> Target time: 356

#> Targets: 9

#> Standardized: FALSE

#> y_old y_new revision

#> gdp 0.0001 0.0001 0.0000

#> priv_cons 0.0000 0.0000 0.0000

#> invest -0.0002 -0.0002 0.0000

#> export 0.0003 0.0003 0.0000

#> import -0.0001 -0.0001 0.0000

#> empl -0.0001 -0.0001 0.0000

#> prductivity 0.5660 0.5803 0.0143

#> capacity -0.8002 -0.8000 0.0002

#> gdp_us 0.0004 0.0004 0.0000

# Data frame with details

as.data.frame(news_qvars) |> na.omit() |> head()

#> target series actual forecast news gain

#> 8 gdp new_cars -0.0002384109 -0.0002167886 -2.162227e-05 7.379485e-04

#> 11 gdp ecs_ec_sent_ind 2.0000000000 1.9544155170 4.558448e-02 7.667486e-07

#> 13 gdp ecs_ind_prod_exp 0.5000000000 2.6387291274 -2.138729e+00 -9.684502e-07

#> 14 gdp ecs_ind_x_orders 1.5000000000 0.9235600067 5.764400e-01 1.336228e-06

#> 16 gdp ecs_cons_conf 3.0000000000 1.4263128445 1.573687e+00 6.372557e-07

#> 20 gdp ecs_serv_empl_exp 1.3999996185 0.6240537062 7.759459e-01 3.695631e-07

#> gain_std impact

#> 8 1.032980e-06 -1.595612e-08

#> 11 1.302062e-06 3.495184e-08

#> 13 -2.125806e-06 2.071253e-06

#> 14 3.272888e-06 7.702555e-07

#> 16 9.474786e-07 1.002841e-06

#> 20 9.496770e-07 2.867610e-07Apart from the overall forecast revision, the news()

function measures, for each series, the impact on the revision, which is

a function of the news (innovation) multiplied by the gain (weight). The

formula impact \(=\)

news \(\times\)

gain always holds, and news \(=\) actual \(-\) forecast holds if there is

only one change to the series between vintages.

dfms also exports central functions that help with DFM

estimation, such as imputing missing values with

tsnarmimp(), estimating a VAR with .VAR(), or

Kalman Filtering and Smoothing with SKFS(), or separately

with SKF() followed by FIS(). To my knowledge

these are the fastest routines for simple stationary Kalman Filtering

and Smoothing currently available in R. The function

em_converged() can be used to check convergence of the

log-likelihood in EM estimation.

dfms also exports a matrix inverse and pseudo-inverse from

the Armadillo C++ library through the functions ainv() and

apinv(). These are often faster than solve(),

and somewhat more robust in near-singularity cases.

dfms provides a simple but robust and powerful implementation of dynamic factors models in R. For more information about the model consult the theoretical vignette.

Other implementations more geared to economic nowcasting applications

are provided in R packages nowcasting and

nowcastDFM.

More general forms of autoregressive state space models can be fit using

MARSS.

For large-scale nowcasting models, the DynamicFactorMQ

class in the statsmodels Python library provides a robust and

performant implementation.

Doz, C., Giannone, D., & Reichlin, L. (2011). A two-step estimator for large approximate dynamic factor models based on Kalman filtering. Journal of Econometrics, 164(1), 188-205.

Doz, C., Giannone, D., & Reichlin, L. (2012). A quasi-maximum likelihood approach for large, approximate dynamic factor models. Review of Economics and Statistics, 94(4), 1014-1024.

Banbura, M., & Modugno, M. (2014). Maximum likelihood estimation of factor models on datasets with arbitrary pattern of missing data. Journal of Applied Econometrics, 29(1), 133-160.

Mariano, R. S., & Murasawa, Y. (2003). A new coincident index of business cycles based on monthly and quarterly series. Journal of Applied Econometrics, 18(4), 427-443.

Bai, J., Ng, S. (2002). Determining the Number of Factors in Approximate Factor Models. Econometrica, 70(1), 191-221.

Onatski, A. (2010). Determining the number of factors from empirical distribution of eigenvalues. The Review of Economics and Statistics, 92(4), 1004-1016.

Stock, J. H., & Watson, M. W. (2016). Dynamic Factor Models, Factor-Augmented Vector Autoregressions, and Structural Vector Autoregressions in Macroeconomics. Handbook of Macroeconomics, 2, 415–525.

Banbura, M., & Modugno, M. (2014). Maximum likelihood estimation of factor models on datasets with arbitrary pattern of missing data. Journal of Applied Econometrics, 29(1), 133-160.↩︎

Both about the monthly ones and quarterly series

contained in BM14_Q. The order of rows in

BM14_Models matches the column order of series in

merge(BM14_M, BM14_Q).↩︎

Data must be scaled and centered because the Kalman Filter has no intercept term.↩︎

Bai, J., Ng, S. (2002). Determining the Number of Factors in Approximate Factor Models. Econometrica, 70(1), 191-221. doi:10.1111/1468-0262.00273↩︎

Onatski, A. (2010). Determining the number of factors from empirical distribution of eigenvalues. The Review of Economics and Statistics, 92(4), 1004-1016.↩︎

Some authors like Doz, Giannone, and Reichlin (2012) additionally allow the number of transition error processes, termed ‘dynamic factors’ and given an extra parameter \(q\), to be less than the number of ‘static factors’ \(r\). I find this terminology confusing and the feature not very useful for most practical purposes, thus I have not implemented it in dfms.↩︎

Users can also choose from two different implementations

of the EM algorithm using the argument em.method. The

default is em.method = "auto", which chooses the modified

EM algorithm proposed by BM14 for missing data if anyNA(X),

and the plain EM implementation of Doz, Giannone and Reichlin (2012),

henceforth DGR12, otherwise. The baseline implementation of DGR12 is

typically more than 2x faster than BM14’s method, and can also be used

with data that has a few random missing values (< 5%), but gives

wrong results with many and systematically missing data, such as ragged

edges at the beginning or end of the sample or series at different

frequencies. With complete datasets, both em.method = "DGR"

and em.method = "BM" give identical factor estimates, and

in this case em.method = "DGR" should be used.↩︎

Doz, C., Giannone, D., & Reichlin, L. (2011). A two-step estimator for large approximate dynamic factor models based on Kalman filtering. Journal of Econometrics, 164(1), 188-205.↩︎

Depending also on the lag-order of the factor-VAR. Higher lag-orders produce more interesting forecast dynamics.↩︎

These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.