gips

The hardware and bandwidth for this mirror is donated by METANET, the Webhosting and Full Service-Cloud Provider.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]metanet.ch.

gips

![]()

![]()

![]()

gips - Gaussian model Invariant by Permutation Symmetry

gips is an R package that looks for permutation

symmetries in the multivariate Gaussian sample. Such symmetries reduce

the free parameters in the unknown covariance matrix. This is especially

useful when the number of variables is substantially larger than the

number of observations.

gips will help

you with two things:gips

can be used as an exploratory tool for searching the space of

permutation symmetries of the Gaussian vector. Useful in the Exploratory

Data Analysis (EDA).From CRAN:

# Install the released version from CRAN:

install.packages("gips")From GitHub:

# Install the development version from GitHub:

# install.packages("remotes")

remotes::install_github("PrzeChoj/gips")Assume we have the data, and we want to understand its structure:

library(gips)

Z <- HSAUR2::aspirin

# Renumber the columns for better readability:

Z[, c(2, 3)] <- Z[, c(3, 2)]Assume the data Z is normally distributed.

dim(Z)

#> [1] 7 4

number_of_observations <- nrow(Z) # 7

p <- ncol(Z) # 4

S <- cov(Z)

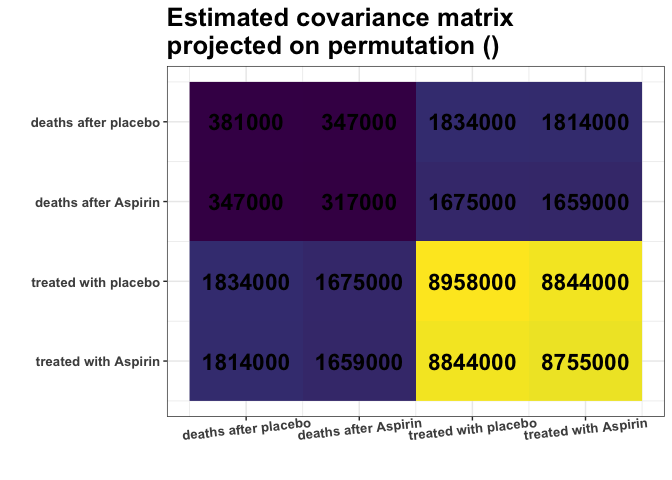

round(S, -3)

#> [,1] [,2] [,3] [,4]

#> [1,] 381000 347000 1834000 1814000

#> [2,] 347000 317000 1675000 1659000

#> [3,] 1834000 1675000 8958000 8844000

#> [4,] 1814000 1659000 8844000 8755000

g <- gips(S, number_of_observations)

plot_cosmetic_modifications(plot(g, type = "heatmap"))

Remember, we analyze the covariance matrix. We can see some nearly

identical colors in the estimated covariance matrix. E.g., variances of

columns 1 and 2 are very similar (S[1,1] \(\approx\) S[2,2]), and

variances of columns 3 and 4 are very similar (S[3,3] \(\approx\) S[4,4]). What is

more, Covariances are also similar (S[1,3] \(\approx\) S[1,4] \(\approx\) S[2,3] \(\approx\) S[2,4]). Are those

approximate equalities coincidental? Or do they reflect some underlying

data properties? It is hard to decide purely by looking at the

matrix.

find_MAP() will use the Bayesian model to quantify if

the approximate equalities are coincidental. Let’s see if it will find

this relationship:

g_MAP <- find_MAP(g, optimizer = "brute_force")

#> ================================================================================

g_MAP

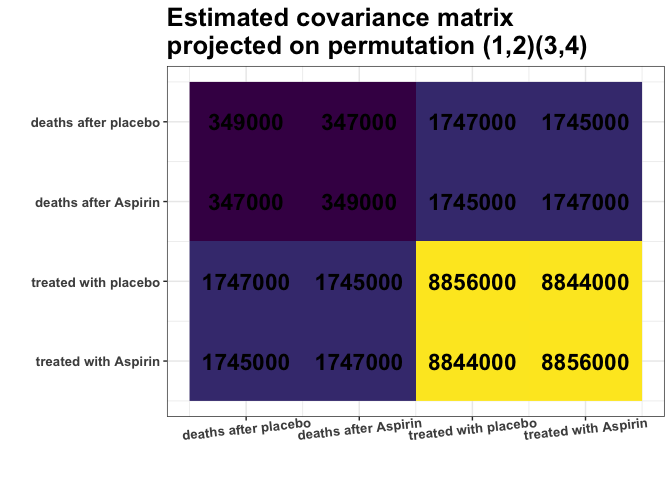

#> The permutation (1,2)(3,4):

#> - was found after 17 posteriori calculations;

#> - is 3.374 times more likely than the () permutation.The find_MAP found the relationship (1,2)(3,4). The

variances [1,1] and [2,2] as well as [3,3] and [4,4] are so close to

each other that it is reasonable to consider them equal. Similarly, the

covariances [1,3] and [2,4]; just as covariances [2,3] and [1,4], also

will be considered equal:

S_projected <- project_matrix(S, g_MAP)

round(S_projected)

#> [,1] [,2] [,3] [,4]

#> [1,] 349160 347320 1746602 1744545

#> [2,] 347320 349160 1744545 1746602

#> [3,] 1746602 1744545 8856368 8844312

#> [4,] 1744545 1746602 8844312 8856368

plot_cosmetic_modifications(plot(g_MAP, type = "heatmap"))

This S_projected matrix can now be interpreted as a more

stable covariance matrix estimator.

We can also interpret the output as suggesting that there is no change in covariance for treatment with Aspirin.

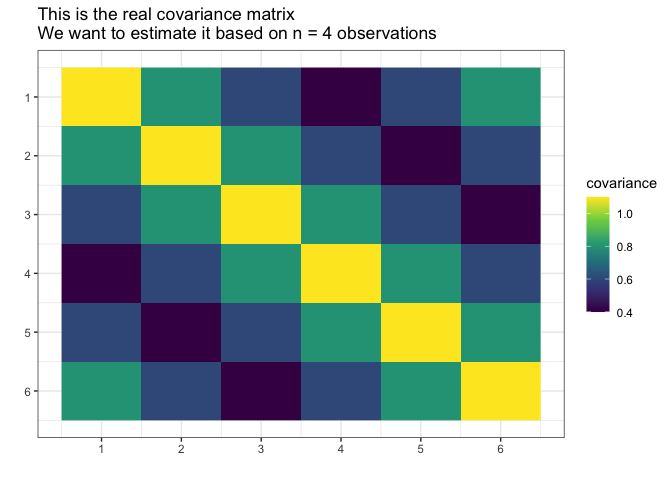

First, construct data for the example:

# Prepare model, multivariate normal distribution

p <- 6

n <- 4

mu <- numeric(p)

sigma_matrix <- matrix(

data = c(

1.1, 0.8, 0.6, 0.4, 0.6, 0.8,

0.8, 1.1, 0.8, 0.6, 0.4, 0.6,

0.6, 0.8, 1.1, 0.8, 0.6, 0.4,

0.4, 0.6, 0.8, 1.1, 0.8, 0.6,

0.6, 0.4, 0.6, 0.8, 1.1, 0.8,

0.8, 0.6, 0.4, 0.6, 0.8, 1.1

),

nrow = p, byrow = TRUE

) # sigma_matrix is a matrix invariant under permutation (1,2,3,4,5,6)

# Generate example data from a model:

Z <- withr::with_seed(2022,

code = MASS::mvrnorm(n, mu = mu, Sigma = sigma_matrix)

)

# End of prepare model

Suppose we do not know the actual covariance matrix \(\Sigma\) and we want to estimate it. We cannot use the standard MLE because it does not exists (\(4 < 6\), \(n < p\)).

We will assume it was generated from the normal distribution with the mean \(0\).

library(gips)

dim(Z)

#> [1] 4 6

number_of_observations <- nrow(Z) # 4

p <- ncol(Z) # 6

# Calculate the covariance matrix from the data:

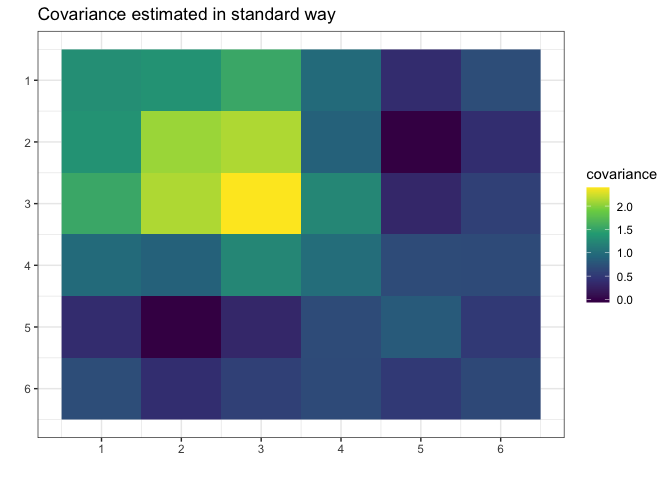

S <- (t(Z) %*% Z) / number_of_observationsMake the gips object out of data:

g <- gips(S, number_of_observations, was_mean_estimated = FALSE)We can see the standard estimator of the covariance matrix: \[\hat{\Sigma} = (1/n) \cdot \Sigma_{i=1}^n \Big( Z^{(i)}\cdot\big({Z^{(i)}}^\top\big) \Big)\] It is not MLE (again, because MLE does not exist for \(n < p\)):

plot(g, type = "heatmap") + ggplot2::ggtitle("Covariance estimated in standard way")

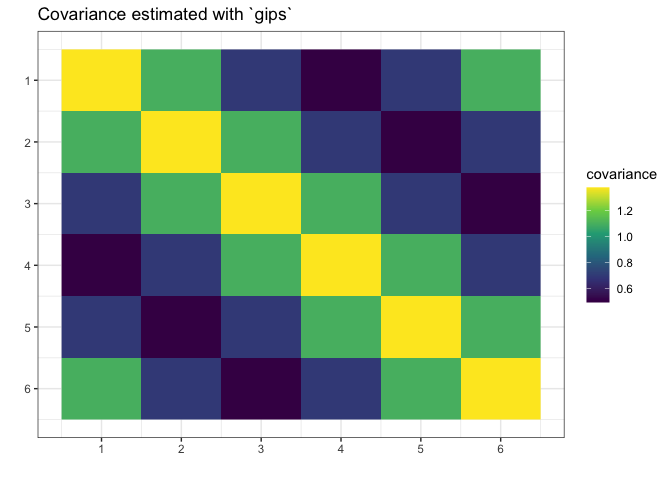

Let’s find the Maximum A Posteriori Estimator for the permutation. Space is small (\(6! = 720\)), so it is reasonable to browse the whole of it:

g_map <- find_MAP(g, optimizer = "brute_force")

#> ================================================================================

g_map

#> The permutation (1,2,3,4,5,6):

#> - was found after 362 posteriori calculations;

#> - is 118.863 times more likely than the () permutation.We see that the found permutation is 118.86 times more likely than making no additional assumption. That means the additional assumptions are justified.

summary(g_map)$n0

#> [1] 1

summary(g_map)$n0 <= number_of_observations # 1 <= 4

#> [1] TRUEWhat is more, we see the number of observations (4) is bigger than or equal to \(n_0 = 1\), so we can estimate the covariance matrix with the Maximum Likelihood estimator:

S_projected <- project_matrix(S, g_map)

S_projected

#> [,1] [,2] [,3] [,4] [,5] [,6]

#> [1,] 1.3747718 1.0985729 0.6960213 0.4960295 0.6960213 1.0985729

#> [2,] 1.0985729 1.3747718 1.0985729 0.6960213 0.4960295 0.6960213

#> [3,] 0.6960213 1.0985729 1.3747718 1.0985729 0.6960213 0.4960295

#> [4,] 0.4960295 0.6960213 1.0985729 1.3747718 1.0985729 0.6960213

#> [5,] 0.6960213 0.4960295 0.6960213 1.0985729 1.3747718 1.0985729

#> [6,] 1.0985729 0.6960213 0.4960295 0.6960213 1.0985729 1.3747718

# Plot the found matrix:

plot(g_map, type = "heatmap") + ggplot2::ggtitle("Covariance estimated with `gips`")

We see gips found the data’s structure, and we could

estimate the covariance matrix with huge accuracy only with a small

amount of data and additional reasonable assumptions.

Note that the rank of the S matrix was 4, while the rank

of the S_projected matrix was 6 (full rank).

For more examples and introduction, see

vignette("gips", package="gips") or its pkgdown

page.

For an in-depth analysis of the package performance, capabilities,

and comparison with similar packages, see the article “Learning

permutation symmetries with gips in R” by gips developers

Adam Chojecki, Paweł Morgen, and Bartosz Kołodziejek, Journal of Statistical

Software.

Project was funded by Warsaw University of Technology within the Excellence Initiative: Research University (IDUB) programme.

The development was carried out with the support of the Laboratory of Bioinformatics and Computational Genomics and the High Performance Computing Center of the Faculty of Mathematics and Information Science Warsaw University of Technology.

These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.