The hardware and bandwidth for this mirror is donated by METANET, the Webhosting and Full Service-Cloud Provider.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]metanet.ch.

The goal is to offer a package that can produce bias-corrected

performance measures for clinical prediction models with binary outcomes

for a range of model development approaches available in R (similar to

rms::validate). There are also functions for assessing

prediction stability, as described in Riley and Collins

(2023).

To install:

install.packages("pminternal") # cran

# or

devtools::install_github("stephenrho/pminternal") # developmentIn the example below we use bootstrapping to correct performance

measures for a glm via calculation of ‘optimism’ (see

vignette("pminternal"),

vignette("validate-examples"), and

vignette("missing-data") for more examples):

library(pminternal)

# make some data

set.seed(2345)

n <- 800

p <- 10

X <- matrix(rnorm(n*p), nrow = n, ncol = p)

LP <- -1 + apply(X[, 1:5], 1, sum) # first 5 variables predict outcome

y <- rbinom(n, 1, plogis(LP))

dat <- data.frame(y, X)

# fit a model

mod <- glm(y ~ ., data = dat, family = "binomial")

# calculate bootstrap optimism corrected performance measures

(val <- validate(fit = mod, method = "boot_optimism", B = 100))

#> It is recommended that B >= 200 for bootstrap validation

#> apparent optimism corrected n

#> C 0.8567 0.0093 0.8474 100

#> Brier 0.1423 -0.0054 0.1477 100

#> Intercept 0.0000 0.0175 -0.0175 100

#> Slope 1.0000 0.0529 0.9471 100

#> Eavg 0.0045 -0.0048 0.0093 100

#> E50 0.0039 -0.0050 0.0089 100

#> E90 0.0081 -0.0107 0.0187 100

#> Emax 0.0109 -0.0057 0.0165 100

#> ECI 0.0027 -0.0038 0.0065 100The other available methods for calculating bias corrected

performance are the simple bootstrap (boot_simple), 0.632

bootstrap optimism (.632), optimism via cross-validation

(cv_optimism), and regular cross-validation

(cv_average). Please see ?pminternal::validate

and the references therein. Bias corrected calibration curves can also

be produced (see pminternal::cal_plot). Confidence

intervals can also be added via confint.

For models that cannot be supported via fit, users are

able to specify their own model (model_fun) and prediction

(pred_fun) functions as shown below. Note that when

specifying user-defined model and prediction functions the data and

outcome must also be provided. It is crucial that model_fun

implements the entire model development procedure (variable selection,

hyperparameter tuning, etc). For more examples, see

vignette("pminternal") and

vignette("validate-examples").

# fit a glm with lasso penalty

library(glmnet)

#> Loading required package: Matrix

#> Loaded glmnet 4.1-8

lasso_fun <- function(data, ...){

y <- data$y

x <- as.matrix(data[, which(colnames(data) != "y")])

cv <- cv.glmnet(x=x, y=y, alpha=1, nfolds = 10, family="binomial")

lambda <- cv$lambda.min

glmnet(x=x, y=y, alpha = 1, lambda = lambda, family="binomial")

}

lasso_predict <- function(model, data, ...){

y <- data$y

x <- as.matrix(data[, which(colnames(data) != "y")])

predict(model, newx = x, type = "response")[,1]

}

(val <- validate(data = dat, outcome = "y",

model_fun = lasso_fun, pred_fun = lasso_predict,

method = "boot_optimism", B = 100))

#> It is recommended that B >= 200 for bootstrap validation

#> apparent optimism corrected n

#> C 0.856 0.0070 0.849 100

#> Brier 0.143 -0.0041 0.147 100

#> Intercept 0.080 0.0191 0.061 100

#> Slope 1.155 0.0449 1.110 100

#> Eavg 0.020 0.0013 0.019 100

#> E50 0.019 0.0026 0.017 100

#> E90 0.040 0.0021 0.038 100

#> Emax 0.044 0.0145 0.029 100

#> ECI 0.053 0.0087 0.044 100The output of validate (with

method = "boot_*") can be used to produce plots for

assessing the stability of model predictions (across models developed on

bootstrap resamples).

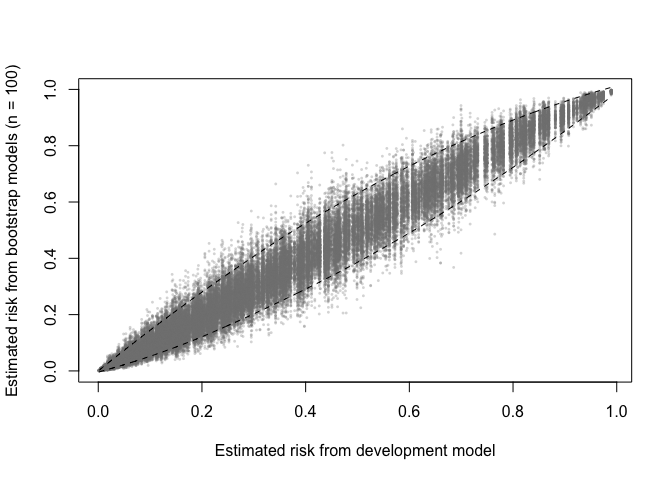

A prediction (in)stability plot shows predictions from the

B (in this case 100) bootstrap models applied to the

development data.

prediction_stability(val, smooth_bounds = TRUE)

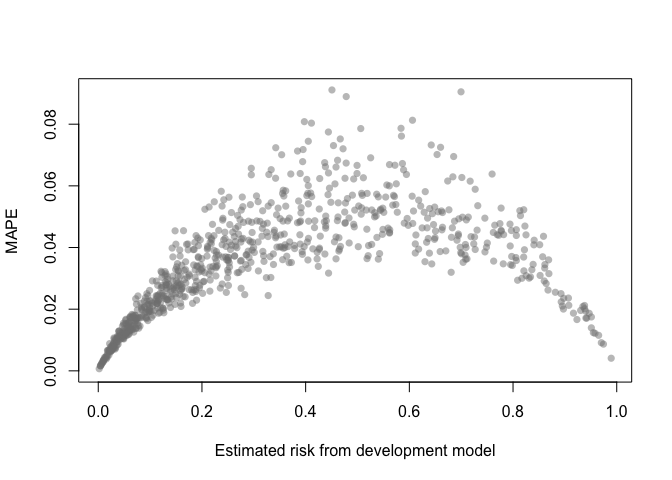

A MAPE plot shows the mean absolute prediction error, which is the

difference between the predicted risk from the development model and

each of the B bootstrap models.

mape_stability(val)

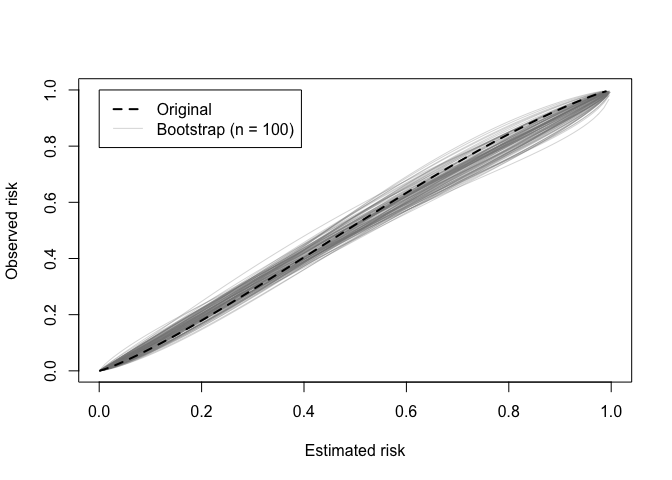

A calibration (in)stability plot depict the original calibration

curve along with B calibration curves from the bootstrap

models applied to the original data (y).

calibration_stability(val)

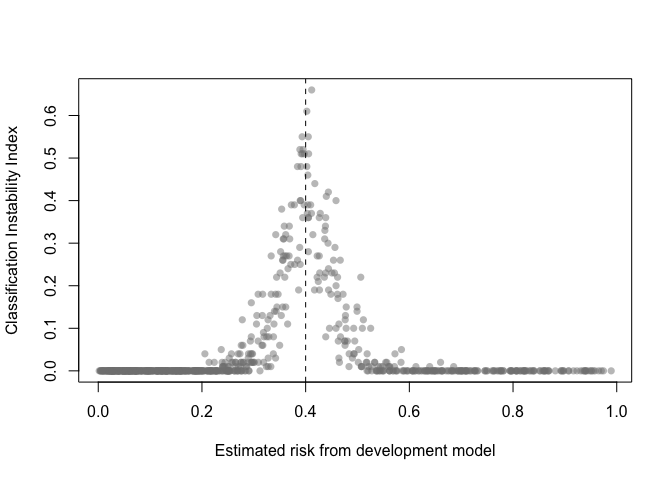

The classification instability index (CII) is the proportion of individuals that change predicted class (present/absent, 1/0) when predicted risk is compared to some threshold. For example, a patient predicted to be in class 1 would receive a CII of 0.3 if 30% of the bootstrap models led to a predicted class of 0.

classification_stability(val, threshold = .4)

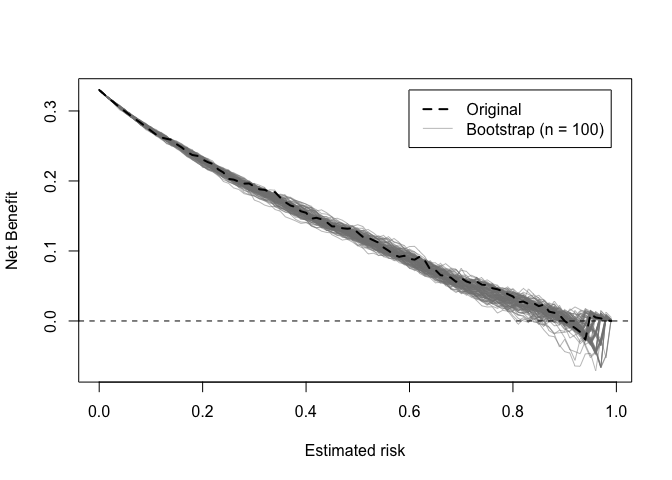

Decision curves implied by the original and bootstrap models can also be plotted.

dcurve_stability(val)

These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.