The hardware and bandwidth for this mirror is donated by METANET, the Webhosting and Full Service-Cloud Provider.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]metanet.ch.

![]()

The goal of tidymodlr is to …

You can install the development version of tidymodlr from GitHub with:

# install.packages("devtools")

devtools::install_github("david-hammond/tidymodlr")This is a basic example which shows you how to solve a common problem with long data:

library(tidymodlr)

data(wb)

head(wb)

#> # A tibble: 6 × 4

#> iso3c indicator year value

#> <chr> <chr> <dbl> <dbl>

#> 1 DZA Population, total 2012 37260563

#> 2 DZA Population, total 2011 36543541

#> 3 DZA Population, total 2010 35856344

#> 4 AGO Population, total 2012 25188292

#> 5 AGO Population, total 2011 24259111

#> 6 AGO Population, total 2010 23364185Here you can see that the format is not conducive to regression or other types of analysis that require wide formats. The indicator names are also long, making pivot_longer result in cumbersome column names. To assist, we build a tidymodl:

mdl <- tidymodl$new(wb,

pivot_column = "indicator",

pivot_value = "value")

print(mdl)

#> Key:

#> key indicator

#> 1 ein Energy imports, net (% of energy use)

#> 2 gcu GDP (current US$)

#> 3 gni Gini index

#> 4 icp Inflation, consumer prices (annual %)

#> 5 ppt Population, total

#> 6 trg Trade (% of GDP)

#> Matrix:

#> # A tibble: 5 × 6

#> ein gcu gni icp ppt trg

#> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 -213. 227143746076. NA 8.89 37260563 60.8

#> 2 -249. 218331946925. 27.6 4.52 36543541 62.2

#> 3 -275. 177785053940. NA 3.91 35856344 63.5

#> 4 -590. 128052915766. NA 10.3 25188292 91.8

#> 5 -619. 111789747671. NA 13.5 24259111 100.This can now be used for regressions

### Use mdl$child for modelling

fit <- lm(data = mdl$child, gni ~ gcu + ppt)

summary(fit)

#>

#> Call:

#> lm(formula = gni ~ gcu + ppt, data = mdl$child)

#>

#> Residuals:

#> Min 1Q Median 3Q Max

#> -11.128 -5.515 1.219 4.132 24.701

#>

#> Coefficients:

#> Estimate Std. Error t value Pr(>|t|)

#> (Intercept) 3.959e+01 1.438e+00 27.523 <2e-16 ***

#> gcu 3.055e-12 9.031e-12 0.338 0.737

#> ppt -4.177e-08 3.828e-08 -1.091 0.282

#> ---

#> Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

#>

#> Residual standard error: 7.589 on 41 degrees of freedom

#> (163 observations deleted due to missingness)

#> Multiple R-squared: 0.03422, Adjusted R-squared: -0.01289

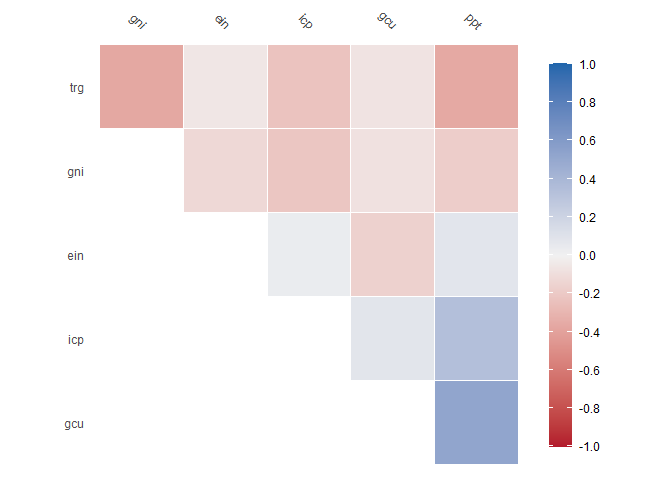

#> F-statistic: 0.7264 on 2 and 41 DF, p-value: 0.4898We can calculate and visualise correlations:

#In built xgboost imputation function

mdl$correlate()

#> Key:

#> key indicator

#> 1 ein Energy imports, net (% of energy use)

#> 2 gcu GDP (current US$)

#> 3 gni Gini index

#> 4 icp Inflation, consumer prices (annual %)

#> 5 ppt Population, total

#> 6 trg Trade (% of GDP)

#> Correlation computed with

#> • Method: 'pearson'

#> • Missing treated using: 'pairwise.complete.obs'

#> # A tibble: 6 × 7

#> term ein gcu gni icp ppt trg

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 ein NA -0.161 -0.123 0.0364 0.0805 -0.0568

#> 2 gcu -0.161 NA -0.0786 0.0810 0.526 -0.0676

#> 3 gni -0.123 -0.0786 NA -0.216 -0.178 -0.367

#> 4 icp 0.0364 0.0810 -0.216 NA 0.341 -0.231

#> 5 ppt 0.0805 0.526 -0.178 0.341 NA -0.364

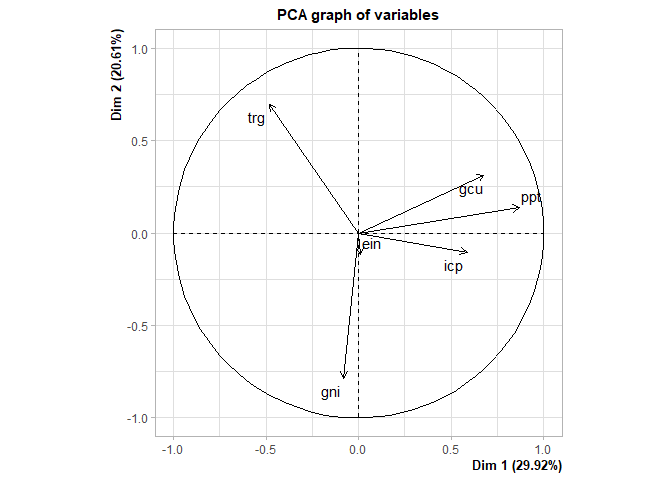

#> 6 trg -0.0568 -0.0676 -0.367 -0.231 -0.364 NAWe can also perform principal component analysis:

# In built principal components analysis function

tmp <- mdl$pca()

#> Warning in PCA(self$child, graph = FALSE): Missing values are imputed by the

#> mean of the variable: you should use the imputePCA function of the missMDA

#> package

plot(tmp, choix = "var")

We can also append any data to the original data frame so long as the

newdata is either:

length(newdata) = nrow(mdl$child)identical(dim(newdata), dim(mdl$child)) == TRUE

### Can be used to add a yhat value for processed data

nc <- ncol(mdl$child)

nr <- nrow(mdl$child)

dm <- nc * nr

dummy <- matrix(runif(dm),

ncol = nc) |>

data.frame()

names(dummy) = names(mdl$child)

tmp <- mdl$assemble(dummy)

head(tmp)

#> # A tibble: 6 × 5

#> iso3c indicator year value yhat

#> <chr> <chr> <dbl> <dbl> <dbl>

#> 1 DZA Energy imports, net (% of energy use) 2012 -2.13e 2 0.541

#> 2 DZA GDP (current US$) 2012 2.27e11 0.220

#> 3 DZA Gini index 2012 NA 0.952

#> 4 DZA Inflation, consumer prices (annual %) 2012 8.89e 0 0.638

#> 5 DZA Population, total 2012 3.73e 7 0.382

#> 6 DZA Trade (% of GDP) 2012 6.08e 1 0.223

### This is useful for imputation purposes as belowThese binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.