The hardware and bandwidth for this mirror is donated by METANET, the Webhosting and Full Service-Cloud Provider.

If you wish to report a bug, or if you are interested in having us mirror your free-software or open-source project, please feel free to contact us at mirror[@]metanet.ch.

![]()

![]()

![]()

This package presents the White’s Test of Heterocedasticity and a bootstrapped version of it, developed under the methodology of Jeong, J., Lee, K. (1999) (see references for further details).

You can install the development version from GitHub with:

# install.packages("devtools")

devtools::install_github("jlopezper/whitestrap")This is an example which shows you how you can use the

white_test and white_test_boot functions:

library(whitestrap)

#>

#> Please cite as:

#> Lopez, J. (2020), White's test and Bootstrapped White's test under the methodology of Jeong, J., Lee, K. (1999) package version 0.0.1

set.seed(123)

# Let's simulate some heteroscedastic data

n <- 100

y <- 1:n

sd <- runif(n, min = 0, max = 4)

error <- rnorm(n, 0, sd*y)

X <- y + error

df <- data.frame(y, X)

# OLS model

fit <- lm(y ~ X, data = df)# White's test and Bootstrapped White's test

white_test(fit)

#> White's test results

#>

#> Null hypothesis: Homoskedasticity of the residuals

#> Alternative hypothesis: Heteroskedasticity of the residuals

#> Test Statistic: 12.88

#> P-value: 0.001597

white_test_boot(fit)

#> Bootstrapped White's test results

#>

#> Null hypothesis: Homoskedasticity of the residuals

#> Alternative hypothesis: Heteroskedasticity of the residuals

#> Number of bootstrap samples: 1000

#> Boostrapped Test Statistic: 12.88

#> P-value: 0.003In either case, the returned object is a list with the value of the statistical test and the p-value of the test. For the bootstrapped version, the number of bootstrap samples is also provided.

names(white_test(fit))

#> [1] "w_stat" "p_value"

names(white_test_boot(fit))

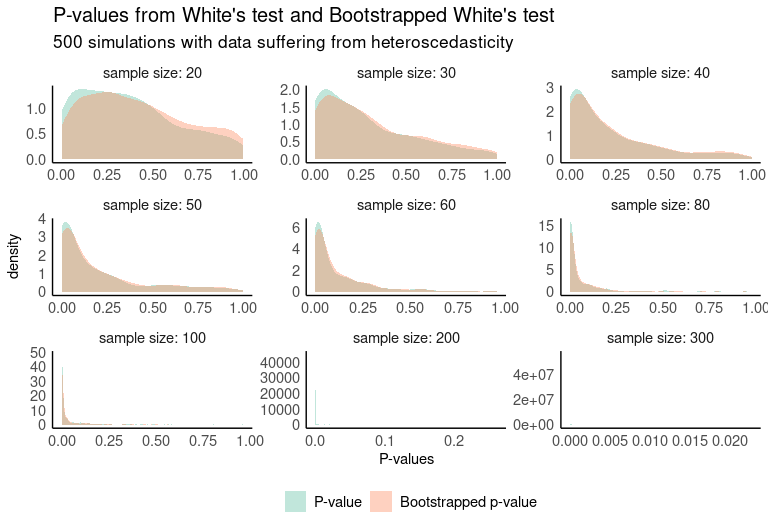

#> [1] "w_stat" "p_value" "iters"One way to compare the results of both tests is through simulations. The following plot shows the distribution of 500 simulations where the p-value of both tests is computed. The data used for this purpose were artificially generated to be heterocedastic, so low p-values are desirable.

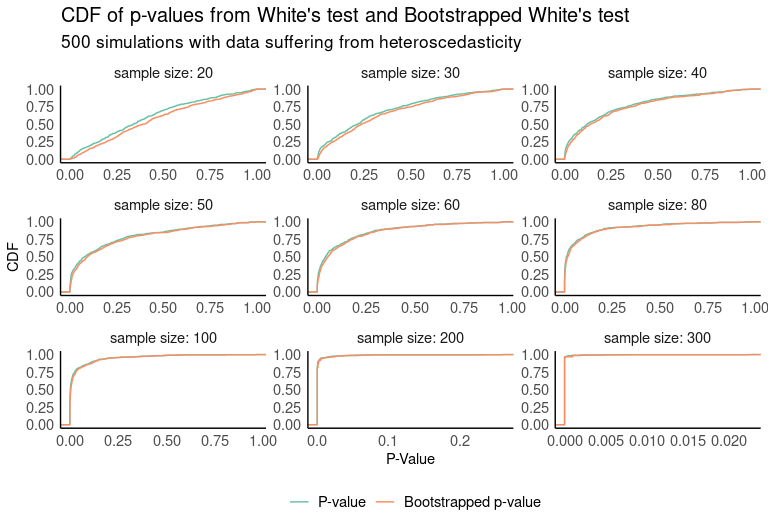

If we look at the cumulative distribution functions of both p-value distributions, we see that in small samples the bootstrapped test returns smaller p-values with higher probability.

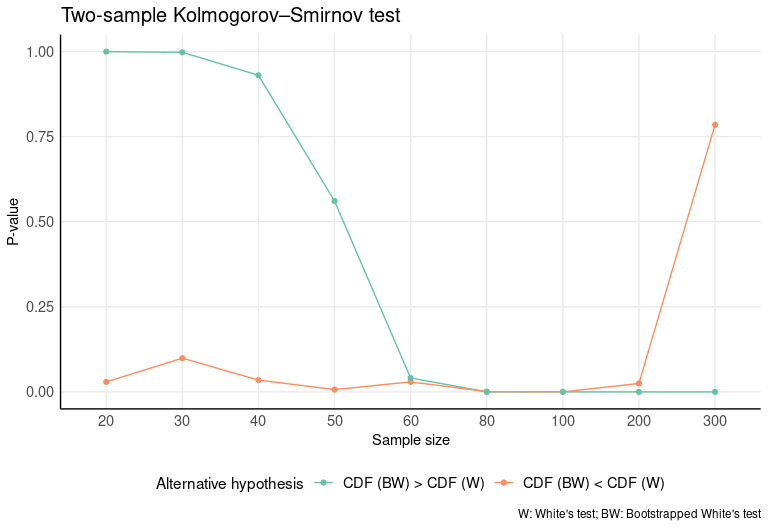

In order to check for differences between the two distributions, a two-sample Kolmogorov–Smirnov test is run. In this case, we’ll test whether one distribution stochastically dominates another, so the test will be run for both alternative sides (CDF (BW) > CDF (W) and CDF (BW) < CDF (W)). We see from the results that CDF (BW) statistically outperforms CDF (W) for samples < 60. No differences are appreciated with samples greater than or equal to 60.

Jeong, J., & Lee, K. (1999). Bootstrapped White’s test for heteroskedasticity in regression models. Economics Letters, 63(3), 261-267.

White, H. (1980). A Heteroskedasticity-Consistent Covariance Matrix Estimator and a Direct Test for Heteroskedasticity. Econometrica, 48(4), 817-838.

Wooldridge, Jeffrey M., 1960-. (2012). Introductory econometrics : a modern approach. Mason, Ohio, South-Western Cengage Learning.

These binaries (installable software) and packages are in development.

They may not be fully stable and should be used with caution. We make no claims about them.